How to Manage Customer Credit in Your Retail Shop and Stop Losing Money in Nigeria (2026 Guide)

SwiftPOS Editorial

Published April 17, 2026

You know this story. A loyal customer walks in, picks out goods worth ₦15,000, and says the familiar words: "Oga, abeg let me owe you till Friday." You agree. Friday comes. Then Monday. Then next week. Then they stop coming entirely — or worse, they come back and ask for more credit before settling the first.

This is the quiet, slow leak that drains hundreds of thousands of naira from Nigerian retail shops every single year. According to Moniepoint's small business research, SMEs account for 96% of all businesses in Nigeria — and untracked customer credit is one of the most consistent reasons cash flow collapses in these businesses.

The good news? Managing customer credit doesn't have to be a nightmare. You don't have to choose between keeping your customers happy and protecting your money. You just need the right rules and the right tools. This guide walks you through all of it — practically, honestly, and with the Nigerian retail reality in mind.

If you've read our earlier article on why your shop is always busy but your account is always empty, you'll recognise that credit mismanagement is one of the core culprits. Let's go deeper.

The Real Cost of Selling on Credit in Nigerian Retail Shops

Selling on credit is not inherently bad. A well-managed customer credit system can build loyalty and drive repeat purchases. The problem is when credit is given without structure — no record, no limit, no deadline, and no follow-up.

Consider this: if your average daily sales are ₦80,000 and even 15% is given on credit without tracking, you're looking at ₦12,000 per day — nearly ₦360,000 per month — floating in customer debts that may never fully return. Multiply that across six months and the number is staggering.

Global retail research from StartUs Insights consistently highlights cash flow management as one of the top three threats to small retailers worldwide. In Nigeria, where economic pressure is sharper and margins thinner, the stakes are even higher.

The losses from unmanaged credit don't just show up as bad debts. They show up as:

- Inability to restock products on time

- Borrowing money to cover expenses that revenue should have handled

- Discrepancies between what your stock says you've sold and what's actually in your hand

- Disputes with customers who claim they've already paid

We explored some of these dynamics in our piece on the true cost of manual bookkeeping for growing retail businesses. Untracked credit is manual bookkeeping at its worst.

Why a Notebook Is Not Enough to Track Credit Sales

Most shop owners use a torn exercise book page, a notebook, or at best a WhatsApp note to track who owes them. While this beats nothing, it fails in critical ways.

Notebooks get lost or damaged — one flood during rainy season and weeks of records are gone. They make it nearly impossible to see your total outstanding credit at a glance. And most dangerously, they can be manipulated by staff. An employee who is close to a particular customer can quietly erase an entry or delay recording a debt.

We wrote a full breakdown of this staff-related risk in our article on how your shop is bleeding money and your staff might be holding the knife. The credit book is one of the easiest places for this to happen.

According to Investopedia's guide on credit management, effective credit control requires consistent documentation, clear terms, and regular review — none of which is achievable through a handwritten ledger in a busy retail environment.

5 Rules Every Nigerian Shop Owner Must Set Before Giving Credit

Before you look at software, you need a credit policy. Without rules, even the best tool in the world won't save you. Here are five rules that successful Nigerian retailers live by:

1. Set a Credit Limit Per Customer

Not every customer should be able to owe the same amount. A customer who has shopped with you for three years and always pays back is different from someone who just started last month. Set a ceiling — for example, ₦5,000 for new customers and ₦20,000 for established regulars — and stick to it. Once a customer hits their limit, no goods leave until they pay.

2. Record Every Credit Transaction Immediately

The moment goods leave your shop on credit, it must be recorded. Not later in the evening. Right then. Whether you're using a notebook or a POS system with a built-in credit module, the record must be instant. Memory is not a system.

3. Set a Repayment Deadline — and Follow Up Before It

"I'll pay on Friday" means nothing unless Friday is recorded as the due date and you follow up on Thursday. State the repayment date clearly when you give credit, make sure the customer acknowledges it, and reach out the day before — not a week after. The longer you wait, the harder collection becomes.

4. Never Stack Credit on Unpaid Credit

A customer owes ₦8,000 from last week but needs more goods today. You feel the pressure and agree. Now they owe ₦15,000, the debt feels harder to bring up, and the number quietly doubles. The rule is simple: settle outstanding credit before any new credit is allowed. No exceptions.

5. Let Payment History Guide Your Decisions

Track your customers' payment behaviour. Someone who pays back reliably within a week is a solid credit customer. Someone who always has excuses is not. A proper retail management system shows you each customer's full history so you decide based on data, not emotion or social pressure.

How to Follow Up on Debts Without Ruining the Customer Relationship

This is where most shop owners struggle. You don't want to embarrass a loyal customer, but you also can't afford to be ignored indefinitely. Here's what actually works:

- Be matter-of-fact, not emotional. "Good morning, just a reminder that the ₦6,500 from last Tuesday is due today" lands far better than an emotionally charged confrontation. Keep it transactional.

- Always follow up privately. Never call out a customer's debt in front of other shoppers. The embarrassment will cost you more in reputation than the debt is worth.

- Remind one day before the due date. A gentle reminder in advance works far better than chasing someone who is already overdue and feeling defensive.

- Accept structured partial payments. If they can't pay the full amount, agree on a partial payment with a clear date for the rest. Something is better than nothing, and it keeps the relationship alive.

- Create consequences for repeat defaulters. If someone consistently misses their repayment date, reduce or remove their credit access — compassionately but firmly. "I'm sorry, I can only do cash for now" is a complete sentence.

The Harvard Business Review notes that the most effective collection strategies combine clear documentation with timely, polite communication. This applies just as much to a retail shop in Lagos as it does to a corporate collections department.

Moving Beyond the Notebook: How the Right Technology Changes Everything

When credit is tracked digitally, several things happen automatically that a notebook can never achieve:

- Every credit transaction is timestamped and tied directly to the specific customer's profile

- You can pull up any customer's complete credit history in seconds

- Total outstanding credit across all customers is visible on one screen at any time

- Staff cannot quietly erase or modify records — every action is logged

- You can set credit limits that the system enforces automatically, so no employee can override your policy

This is the difference between hoping your credit system works and knowing it does. Our guide on how SwiftPOS works as a complete retail management system shows how all these pieces connect into a single daily workflow.

According to Forbes Advisor's breakdown of POS system benefits, businesses that implement proper point-of-sale and customer tracking software report significantly fewer unrecorded transactions and dramatically better cash flow visibility — both of which directly cut credit losses.

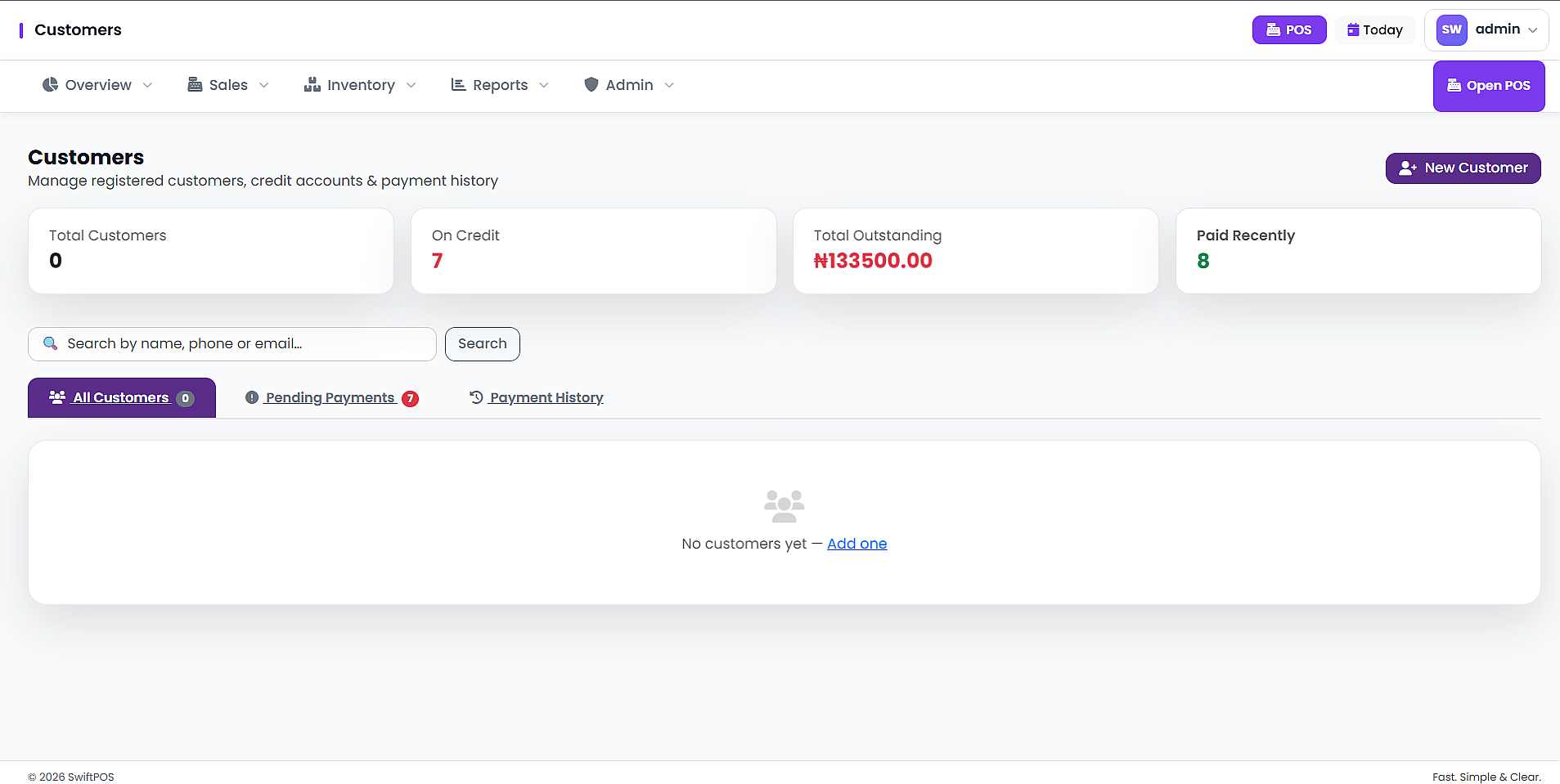

How SwiftPOS Handles Customer Credit Automatically

SwiftPOS is a cloud-based retail management system built specifically for Nigerian businesses, with a dedicated customer credit tracking module. Here's what it gives you:

- Customer profiles — every customer has their own record with name, contact information, and full purchase history

- Instant credit logging — credit sales are recorded at the point of sale and tied directly to the customer's profile

- Individual credit limits — you define how much each customer can owe before the system flags or blocks further credit

- Outstanding balance dashboard — see the full list of customers and exactly what each one owes, at any time

- Full payment history — every repayment is logged, so you always know where each customer stands

The SwiftPOS customer management screen — track every customer's credit balance and payment history in real time.

This is especially valuable if you run a supermarket, a provision store or mini mart, or any shop where you serve the same customers repeatedly. You build real data on who your most reliable — and most problematic — credit customers are.

If you're also dealing with inventory losses, read our related piece on stock management for small businesses in Nigeria — credit losses and inventory losses tend to compound each other, and addressing both together multiplies the impact.

What Does It Cost to Get This System for Your Shop?

SwiftPOS plans start from ₦3,000 per month — less than the cost of a single unrecovered credit sale for most shops. Here's the full breakdown:

| Plan | Price | Customers Supported | Key Highlights |

|---|---|---|---|

| Starter | ₦3,000/month | Up to 100 | POS terminal + customer credit system + inventory |

| Standard | ₦6,000/month | Up to 1,000 | Full P&L reports + audit logs + barcode scanner |

| Pro | ₦12,000/month | Unlimited | Multi-branch + suspicious activity detection + custom branding |

All plans include 1 month free when you subscribe annually. See the full breakdown at the SwiftPOS pricing page.

Credit Management Is Record Keeping — And Record Keeping Is Business Survival

The shops that survive long-term in Nigeria are the ones that know exactly how much money they have, how much they've sold, and how much is owed to them — at any given moment. The shops that slowly drain away are the ones that run on memory, gut feeling, and hope.

We've written at length about this in our post on why every retail shop in Nigeria needs proper record keeping in 2026. Customer credit is one of the most neglected parts of that equation.

The U.S. Small Business Administration's financial management guide states clearly that tracking receivables — money owed to you — is just as important as tracking your sales. Credit given and never properly recorded is revenue that exists only on paper, and paper doesn't pay your suppliers.

Frequently Asked Questions About Customer Credit in Nigerian Retail

Should I stop giving credit altogether?

Not necessarily. Credit is a relationship tool deeply embedded in Nigerian retail culture, and cutting it off entirely can push loyal customers to competitors. The goal is not to eliminate credit but to control it — with clear rules, proper records, and the right tools.

What should I do when a customer simply refuses to pay?

Start with calm, private communication. Remind them of the amount and the agreed date. If they continue to avoid it, reduce or remove their credit access immediately. For very large amounts, some shop owners involve a trusted community mediator. Accept the loss if necessary — and ensure that customer never receives credit again.

How many credit customers can I realistically manage?

With a notebook, realistically 10–20 before it becomes confusing. With a POS system like SwiftPOS, you can manage hundreds or thousands of credit accounts — all organised, searchable, and updated in real time.

Can my staff manage customer credit when I'm not around?

Yes — but only if you have a system that logs who approved each transaction and enforces your credit limits automatically. SwiftPOS logs every staff action, giving you a full audit trail even when you're not present. Read more in our guide on how to stop staff theft in your retail store.

What is a healthy level of outstanding customer credit?

A common guideline is to keep total outstanding credit below 10% of your monthly revenue. If the number climbs higher, it starts putting real pressure on your cash flow. Monitor this regularly through your POS dashboard and act quickly when it rises above your threshold.

Ready to Take Control of Your Customer Credit?

If you've been using a notebook, a WhatsApp message, or just your memory to track who owes you money, today is a good time to change that. The difference between a shop that grows and one that slowly loses ground is rarely the volume of sales — it's the discipline in how money is tracked, collected, and reinvested.

SwiftPOS gives you a complete retail management system with a built-in customer credit module, staff management, inventory tracking, P&L reports, and more — starting at just ₦3,000 per month.

👉 View the pricing plans here and find the right fit for your shop.

📲 Or message us directly on WhatsApp: +2349164601810

Subscribe annually on any plan and get 1 month completely free.

Also worth reading from the SwiftPOS blog:

- How Poor Inventory Management Is Costing Your Supermarket — and How to Fix It

- Point of Sale Software in Nigeria: What the Best Retailers Know That You Don't

- The 7 Best POS Systems for Small Businesses in Nigeria — 2026 Guide

- Is Supermarket Business Profitable in Nigeria? Costs, Risks & Real Profit Insights